Deep(ish) Dive on Intercure ($IRCLF)

Deep(ish) Dive on Intercure ($IRCLF)

I may be right, I may be crazy...

This post will be different than my others thus far, but I stumbled into Intercure while researching US cannabis plays and wanted to organize my thoughts. In doing so, I figured I might as well make them public so folks can tell me where I have gone awry and or benefit from what I’ve pulled together. As always, this is not investment advice / do your own due diligence. Disclosure: position $IRCLF

Intercure

When you google Intercure the first result tells you:

“ InterCure is a medical device company focused on respiratory treatment that has developed and patented a technology platform.”

Odd, you might think, given the introduction mentioned cannabis. Indeed, peeling back the layers on this is a bit convoluted. My thesis (thus far) is that might lead, in part, to an opportunity.

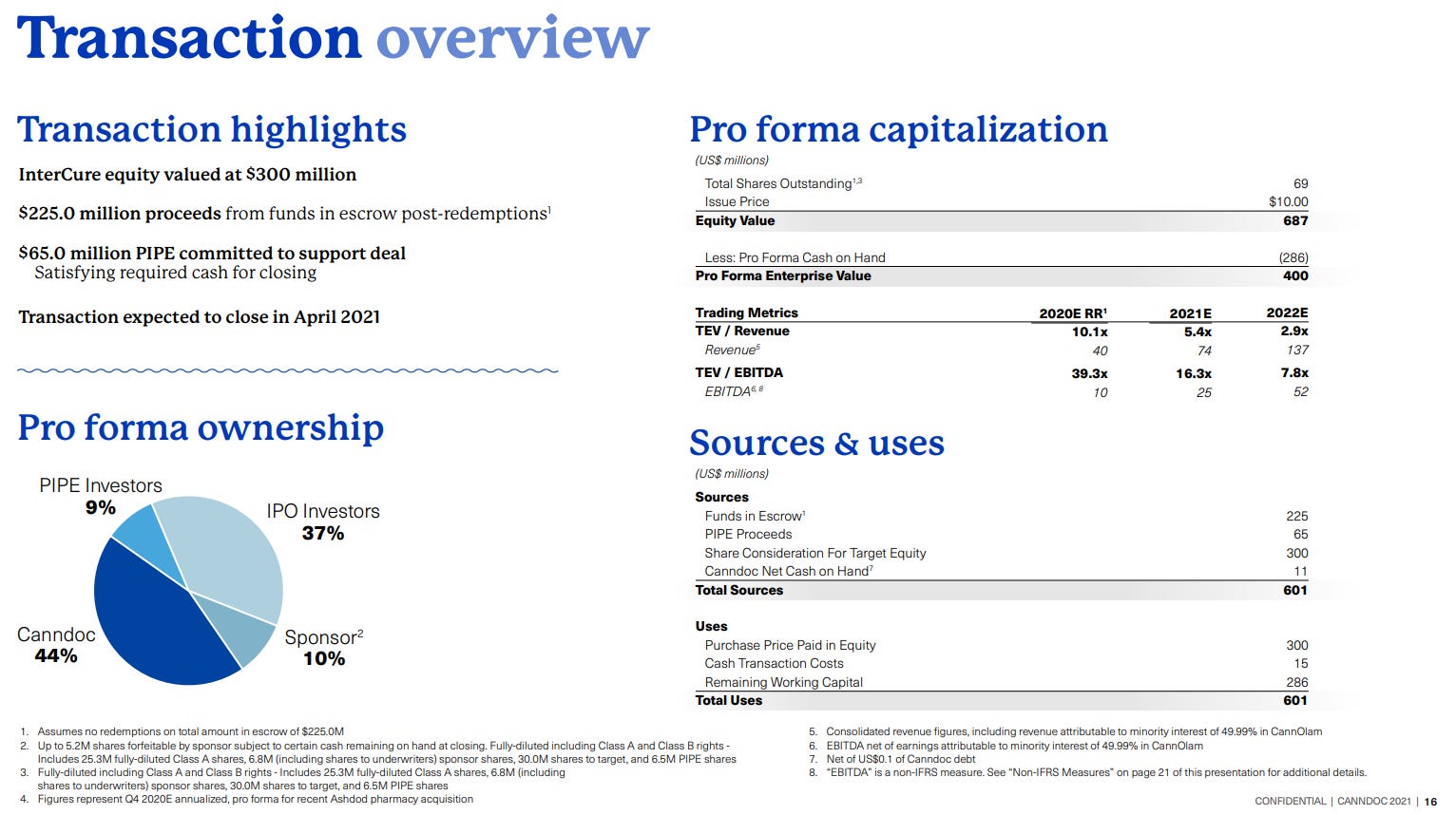

So how does Intercure intersect with cannabis? Intercure owns a subsidiary company, Canndoc, (Canndoc represents 99 percent of Intercure). Canndoc (and thus Intercure) are currently under agreement to be combined with Subversive Capital via their second SPAC, the Subversive Real Estate Acquisition REIT ($SBVRF) at a valuation of $300M USD (the first subversive SPAC ($SBVCF) is now The Parent Company (ticker: $GRAMF), the California cannabis play backed by Jay Z and other big names).

This part is somewhat confusing, too, because though the new SPAC has ‘REIT’ in its name - this obviously is no longer a REIT play. The SPAC was formed with the idea the target would be a REIT and had a deal in place for a REIT before it fell through for ‘technical reasons’.

Thus far, not that interesting but certainly fairly confusing. Where my interest is piqued is Intercure is actually already a publicly traded company in Tel Aviv. As of writing it appears it trades somewhere between about $1.85 and $2.00 USD which, if my math is correct puts the market cap between $220 and $240 mil.

Looking at the prospectus you can see Intercure is being valued at $300 million. The combined entity will have an equity value of $687 million of which 44% will be owned by current Canndoc/Intercure investors (687*0.44 = ~300). The combined company will be sitting on a pile of cash that can be used for acquisitions, expansion, etc.

So the question becomes, to me, how does this disconnect end up shaking out and is their an opportunity here?

Mechanically, I believe what is going to happen is up to the transaction $IRCLF is going to continue trading over the counter. Upon closing, the combined company will trade on the Nasdaq as $INCR. It isn’t 100% clear to me what will happen to the OTC shares - I would imagine they get converted to $INCR, but that’s not explicitly stated anywhere I can find. Listing on the Nasdaq is a requirement of the transaction. I’m no expert on the matter, but since the company is not operating in the US I believe this shouldn’t be an issue.

The deal is expected to close in April. There seems to be two ways this shakes out. One, as we get closer and the deal becomes more certain - $IRCLF trades up closer to the $300 mil valuation. Alternatively, the deal closes and the new combined company immediately trades down like 33%? I don’t even know mechanically how that would happen so my best guess is that as we get closer to April $IRCLF begins creeping closer to $2.50 which would be the share price at the $300 million valuation.

Also should note for those who like following the current hotness ($ARK…) their Israeli innovation fund picked up Intercure and it’s a top 5 holding.

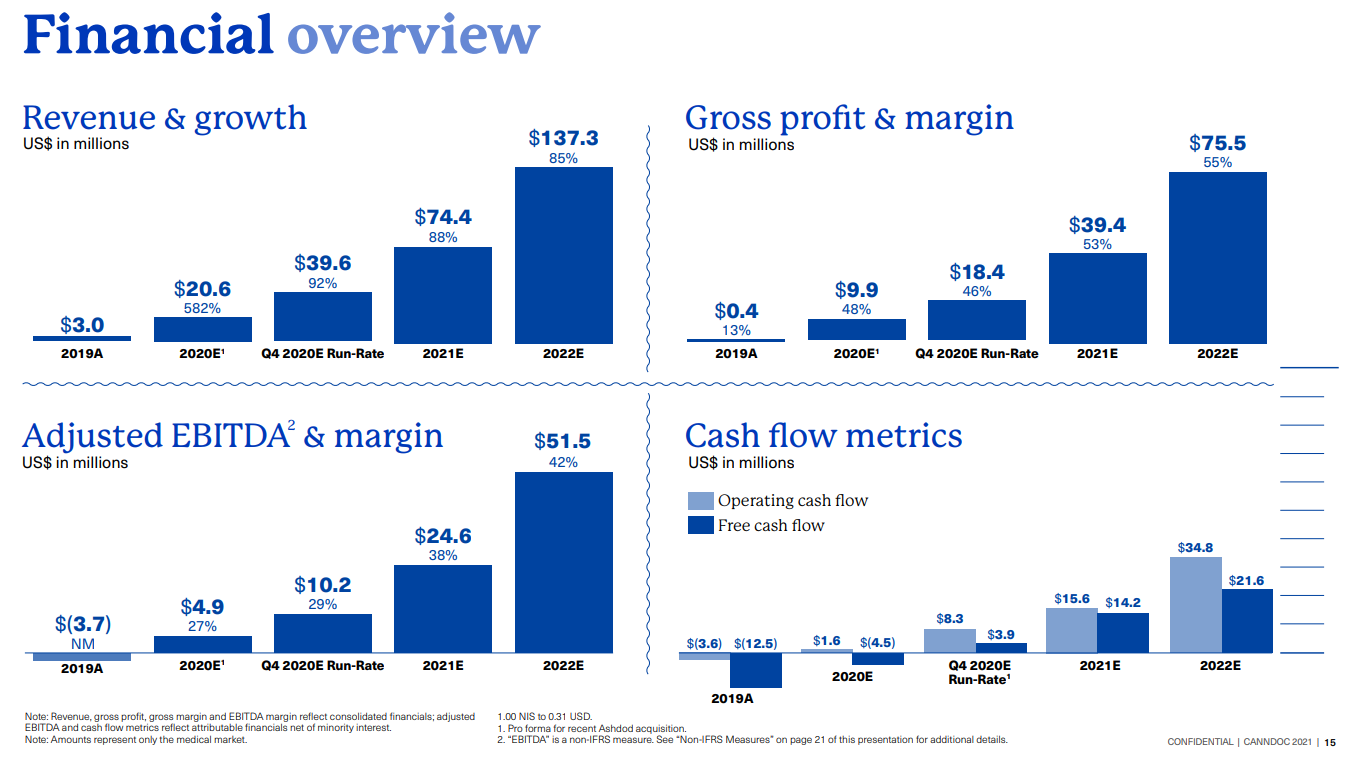

The biggest risk to this trade, I think, is the deal falling apart and Intercure going back to pre-agreement levels. Let’s call that around $1.00 USD and $100 million or so market cap. Per the investors deck estimates for 2021 are $25 mil in EBITDA which though likely somewhat aggressive, seems reasonable. Even without the transaction, this feels closer to a $2-$3 stock, especially considering the macro tailwinds in cannabis’ favor.

The second biggest risk is I don’t actually understand how the fundamentals of the deal will shake out. Hopefully if that is the case someone will enlighten me after reading this.

Finally, as I’ve noted most of my “due diligence” if we can call it that is combing through Twitter for ideas from people smarter than me. Usually if you search a ticker there will be a good amount of tweets relating to it (even after filtering out all the bot noise who spam tickers). Searching $IRCLF is basically a ghost town. So, either everyone is indeed smarter than me and took a look at passed, or it’s an underrated/underappreciated opportunity.

TLDR:

Intercure ($IRCLF) at $1.85-$2:00 presents an interesting opportunity due to the impending combination with ($SBVRF). The underlying business itself seems investable so even if the deal falls through I am not left with something ‘worthless’ though will likely have to hold / average down a bit at that point.