To Sell or Not to Sell

That is the question...

Everyone’s favorite lumber baron came out with a thread today on selling discipline today that caught my eye and had me thinking. He broke down the reasons for selling into two (fairly broad) categories:

This post was in response to another great thread by Elliot Turner where he discussed some of his failures in “overstaying his welcome” and some of the reasons he has done so:

As those who follow along this Substack and/or my twitter feed likely know, my due diligence isn’t exactly…great. My entire thesis is an exercise in what everyone says not to do: “borrow conviction from folks smarter than me”. In this post I’m going to take a run through my current portfolio and try to put some rails around current holdings (ignoring some of the YOLO call spreads which are mostly binary bets) & attempt to describe both the thesis and where I would be a seller. Yes, I am aware this was supposed to happen before I bought, sue me.

$ICLTF

First, it’s genuinely hilarious to me that this random lumber company is my largest position. Perhaps even more enjoyable is 29,000 out of my 30,000 shares aren’t even in my account so it’s almost like the position doesn’t exist! I put the trade (er, investment) on when my account was….higher…and it’s held up better than a lot of things hence the large weighting at present.

Thesis: lumber prices are going to stay higher for longer for a myriad of reasons (housing demand & undersupply, climate related supply shocks to lumber, etc).

Most of my work here has been done by other people. I generally refer back to this article from Twebs when thinking through valuation and I’ve included my favorite table from that piece below:

If the shares were in my account I’d sell half my holdings at $3 and free roll the rest. I don’t expect price to move that much, but I am happy to let these sit and watch the market unfold over the next 2-3 years.

$MSOS Calls

Thesis: US multi state operators are fundamentally undervalued due, primarily, to the lack of ability for institutional investors to participate in the space.

I own a bunch of Leaps (Jan ‘23 and Jan ‘24) across various strikes on $MSOS.

All of the above were originally put on as call spreads, but I have bought back quite a few of the calls I sold during the last week or so and also rolled down my strikes a bit. There are a few moving parts here.

For the Jan ‘24 45 calls I have sold I’d buy those back at $3 if it gets back down there.

Anything above $6 and I’d start looking to sell them again - ideally would be selling at ~$7.50. I’m hopeful the broader market keeps from having the bottom fall out and if we get another bump on legislative chatter (SAFE, etc.) I’ll have another chance to sell the rip and then let the spreads ride.

I’d also like to roll down the ‘24 35’s a bit further if given the opportunity. Generally would buy the 25’s and sell the 35’s if I can do so for < $2.

For the Jan ‘23 calls - I’d like to roll my 45s down soon if I can get a decent price on the $25s. Then, again, would be looking for a spike to perhaps sell $35s if we get a good pop. Those were as high as ~$8 in December during the last mini-run.

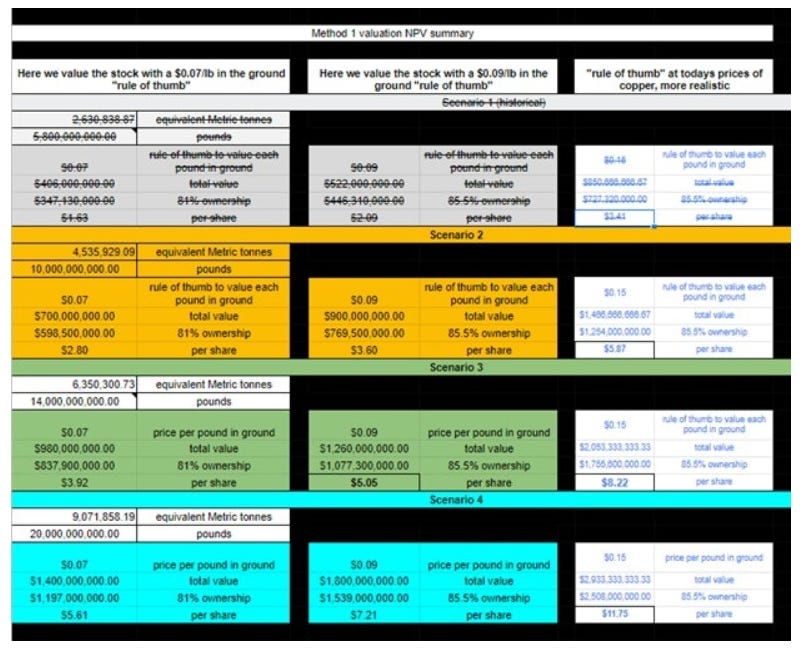

$ORRCF | $OCO.V

Thesis: copper is expensive and there aren’t many big viable projects in waiting.

I’ve written about when I’d sell this one in the past and noted I would be a seller at $3 (before the drilling program started). I held true to that and though it didn’t exactly hit $3 I sold a chunk of my holdings in the high 2’s in mid 2021. The good news is that this is now an entire free-roll which mentally has made it pretty easy to live through the ~50% drawdown since. This post by Ney Torres H (@ney123456789) illustrates a view ways to go about valuing the opportunity at this point. What I’d consider the ‘easiest’ method and thus the way that appeals most to me is just copper in the ground times a per pound price.

Mariusz (classic value investor) has also taken a stab at valuation (albeit a bit old at this point), that’s worth a listen - at the end he quotes $1-$1.5B as his target. Given I’ve sold enough to cover my cost & turn a little profit I fully expect to just hold this one until there is an exit event in ~2 years. If the stock was at $5 now, I’d sell, but I’d imagine if we get to $4.50 there will be additional data around the drilling program and/or copper prices that could change the calculus.

$MX

Thesis: They had the company sold for $29 and got another offer for mid 30’s. Sale was blocked so they picked up ~$1.50 in cash. All signs point to them trying to sell again and I can’t imagine them settling for less that $29.

Given2Tweet (locked account) is the expert on the name for me. Most recent YouTube video is here.

If you gave me $27.50+ today I’d sell. Otherwise, just waiting for them to get bought.

$GLASF

Thesis: cannabis, again. Same as $MSOS with the twist that I love the greenhouse asset, Graham seems like a beast, and Aaron always manages to bull me up (his thesis is here). See the part that excites me the most below:

If nothing changed and you gave me $10 right this second I’d probably sell, but if we get some visibility into Cali firming up a bit and the greenhouse coming along that number will go way up.

One of the favorite things I’ve seen re: when to sell these companies is something along the lines of “wait until the tickers are less than 5 characters” - which resonates with me.

$AYRWF

Thesis: cannabis, again. But this time undervalued compared to peers (which are already undervalued). See comps here.

I’ve taken profits in this name so I think close to a free roll and it was my first ever cannabis stock, so has a sentimental place in my heart. I plan to hold this thing until they get bought, management changes, or uplisting happens.

$MYOV

Thesis: Sheep likes it and I’m pissed I wasn’t bigger in $UROV before they got bought.

I have no real edge here other than being able to be patient and wait for a potential buyout. I’d unload half at $24 at this point if offered and will likely sell OTM calls over the next few months on half my holdings just for kicks. Sumitomo was buying up to $25 if memory serves.

$VRNOF

Thesis: Ah, yes, more cannabis. Again, very cheap compared to an already undervalued sector.

I’d be more inclined to sell this than $AYR because I haven’t been following it as closely and I have less attachment to it. Would be inclined to sell half if we hit $20 - which would be ~15x ‘22 estimated EBITDA.

$PLGNF

Thesis: Mobile casino gaming is a high growth sector and Playgon, via their Vegas live dealer mobile-first technology, is well situated to take advantage if they can execute. If growth stalls the thesis is busted.

This one admittedly is a bit of a yolo bet. I’d sell for $0.50 cents given what I know now - but my guess is we don’t see that number until we get some more information on growth & paths to profitability so I’m just hanging on to my shares. Generally a buyer around $0.15 if we crash down back there for whatever reason.

$UWMC

Thesis: The meme below from Mike sums it up well. Additionally, at current prices you are getting ~8% divvy yield to see how things go. Rudimentary analysis seems to indicate they can keep paying that even as business slows down in a rising rate environment (though if you believe the company they will do better than peers in such an environment where the main driver is new purchases).

I’m highly content just sitting back and collecting my divvy - I’d sell right now at ~$10. New information sure to change that. I think the CEO is bit of a wild card which I like - wouldn’t be shocked if they do a special dividend or something. Idea originally came from Andrew at YAVB and I’ve been monitoring it since. Think it’s an attractive play at these levels.

$XERS

Thesis: The current biotech tape is awful, my brother likes it, and it just seems terribly cheap. Gvoke keeps chipping away at market share.

Small position so I’m content just waiting it out. I’d sell at $5 or so given what we know now. Don’t anticipate that short-term, but hopefully they put together a few good quarters.

$POSAF

Thesis: Another cannabis play, shocking I know. Thesis here is a “picks & shovels” software play serving the legal industry. It’s growing like crazy, but undervalued due to both the general undervaluation of most cannabis-adjacent opportunities as well as being listed on a terrible exchange. Jeremy has a great write up here as well as a podcast episode discussing the thesis here. Thesis would be busted if growth slows materially (would need to see it under the rule of 40).

Quoting from the article - Jeremy summarizes: “In sum, I think 10x EV/revenues on 2022E numbers is a very reasonable back-of-the-envelope starting point considering the scope of the opportunity here - and on that basis the stock, on my numbers, would be a $4.5 CAD stock (>2.5x higher than current).” That’s about $3.50 USD which would be a great return and I’d sell there today. Don’t expect to reach that level until we have more concrete visibility into ‘22 actuals at which time my price might increase.

$INCR

Going to save this one for another post because it’s probably the name I’ve done the most “original” work on so want to flesh it out more properly.

In Summary

This felt like a worthwhile exercise and is likely something I will come back to quite a bit as we navigate the chop & volatility of 2022.